Multifamily companies are using more and more technology, and it’s touching more and more areas of property operations. Most of the time it improves experiences and makes things more efficient. We tend to think about its impact on operations, costs, performance and customer experience. But as with most things, there can be unintended consequences.

As technology proliferates, the cost of technology increases too. In this article, I will focus on one cost in particular: the administrative overhead associated with decision-making. It appears to be growing in many multifamily companies, and it is becoming harder to control. As I will explain, there are important implications for both operators and vendors.

A Couple of Data Points

Over the last few years, the annual 20 for 20 survey has acted as a temperature check on the industry. Each year I interview 20 COOs and heads of IT to understand their priorities in operations and technology. It’s provided an opportunity to see what’s changing in the industry. And over the last few years, it has provided a couple of interesting data points about the cost of innovation.

Two years ago, almost all respondents had reported having formalized a corporate process for innovation. It seemed to be a consequence of the increase in VC dollars finding their way into multifamily technology. More investment meant more technology to understand and more evaluations to do. The industry’s traditional technology gatekeepers sounded overloaded with keeping track of the expanding technology stack.

This year’s report, which came out in February, found something much more specific. While the flow of capital, the pace of innovation, and the scope of technology continue to accelerate, the technology decision processes seem to be changing. In particular, the definition of “technology gatekeepers” appears to be expanding.

What Prioritization Tells Us

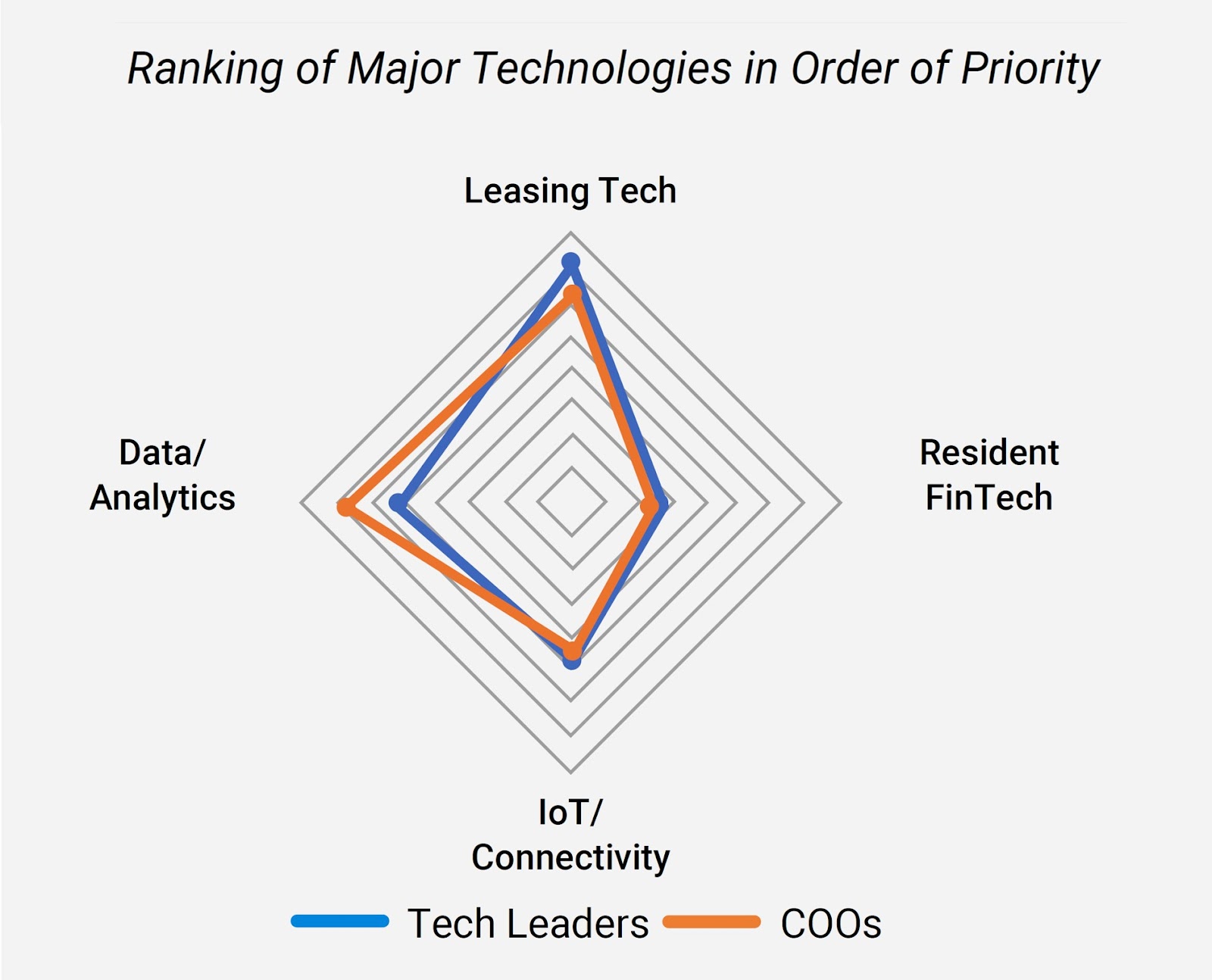

In this year’s research, we split the tech stack into four discrete segments: Leasing Tech, Data Analytics, IoT/Connectivity, and Resident FinTech. We asked each of the 20 respondents to rank the four segments in order of priority. The results, which we summarized in the chart, are instructive.

Leasing was unsurprisingly the top priority; after all, it is the area that has changed the most over the last couple of years. Data analytics was highly active as the pandemic forced management teams to virtualize and report on many new metrics. But it is the two lower-priority technology segments that are more surprising.

IoT should be a higher priority than it is, given the high costs and the risk inherent in installing physical equipment into properties. That it sits in third place probably has more to do with decision processes than its actual importance.

Consider the way that companies buy technologies like access control. It’s normal for the traditional technology buyer (the CIO or the CIO) to be heavily involved in deciding which technologies they will support in their companies. But the actual decision to purchase the technology is much more of a property-by-property decision.

So it may start as a decision that looks like a traditional technology selection process, overseen by the traditional technology gatekeepers. But then it changes into something far more like the decision to renovate a property or purchase appliances.

A similar thing is at play with Resident FinTech: a fast-growing segment of the tech stack, with numerous new companies and innovations taking hold in the industry. These tools are both popular and relatively easy to implement, so evaluation and decision-making are frequently delegated in the organization. Numerous CoOs, for example, described being aware of the fintech that tech companies were buying and implementing but had delegated decisions to buy it and implement it.

What This Means for Operators

More tech can simplify and remove friction from operations, which is a great thing, but it creates different types of complexity. The risk is that when firms delegate decisions below to traditional gatekeepers, they risk creating “shadow” IT departments, where decisions are made outside of the control of corporate IT.

Deposit Alternatives provide a good example: a quick look at the websites of competing suppliers shows that they include the same companies as clients. Vendors appear to be succeeding in selling directly into regionals, for example. And this has implications for vendor management and customer experience because having many different vendors across different regions makes it harder to offer consistency across a portfolio.

In the case of IoT, devolved decision-making can drive up IT costs. Non-IT actors (e.g., Asset Management) are making decisions to implement technology like access control in a particular asset. That makes sense, as the asset manager is responsible for allocating capital to the property, but their decisions can impact IT overhead, a pool of costs that it is not their job to manage.

That represents risk. Imagine choosing to roll out an access control solution means contracting with multiple vendors rather than a single provider. That creates a level of overhead, training, contract management, misaligned agreement dates, and general admin overhead that companies should want to avoid. As decisions like this become more devolved, the risk of higher overhead will increase.

What it Means for Technology Vendors

Vendors need to be aware that the bull’s eye is moving. It’s always been a winning strategy to focus on the traditional gatekeepers, the COOs and heads of technology. (That’s why 20 for 20 focuses on those specific roles!) But in my work, I’m increasingly seeing vendors lose business to competitors who did a better job of figuring out who is making the decisions.

The losing sales teams focus on selling into the conventional buyer persona, while the vendor that won the businesses figured out where the real influence was. It’s particularly true in companies whose sales teams do not yet have deep insight into the multifamily industry.

The mistargeting of effort filters through to marketing activities too. I work with many marketing departments across the tech sector, but I can think of very few who apply significant effort to persona-based marketing campaigns.

As technology and decision-making proliferate, this (already substantial) opportunity will continue to grow. More companies should grasp it! Companies need a wider variety of playbooks to integrate a more sophisticated concept of personas. It will confer an increasing advantage on the companies willing to invest in being good at it.

Unintended consequences aren’t always harmful. It is easy to think of ways that devolved decision-making improves multifamily operations as teams get smarter about how technology improves resident and associate experiences. But operators and vendors should be wise to this changing landscape. Administrative overhead is easy to ignore until it isn’t! And sales and marketing playbooks should always reflect the current state of our industry.